- 12 Mar

- 2025

PERBANDINGAN LSTM, GRU DAN Bi-LSTM UNTUK PREDIKSI HARGA SAHAM PADA TIGA SEKTOR INDUSTRI INDONESIA

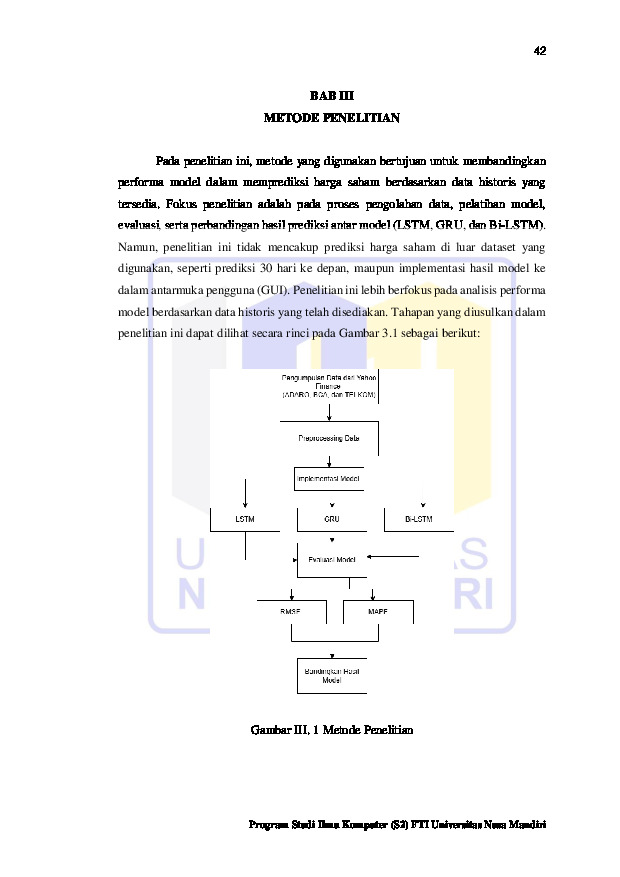

Prediksi harga saham di pasar modal Indonesia merupakan tantangan signifikan akibat

volatilitas yang tinggi. Penelitian ini bertujuan untuk membandingkan performa model

deep learning, yaitu Long Short-Term Memory (LSTM), Bidirectional LSTM (Bi

LSTM), dan Gated Recurrent Unit (GRU), dalam memprediksi harga saham di tiga

sektor industri: energi (ADRO), perbankan (BBCA), dan telekomunikasi (TLKM).

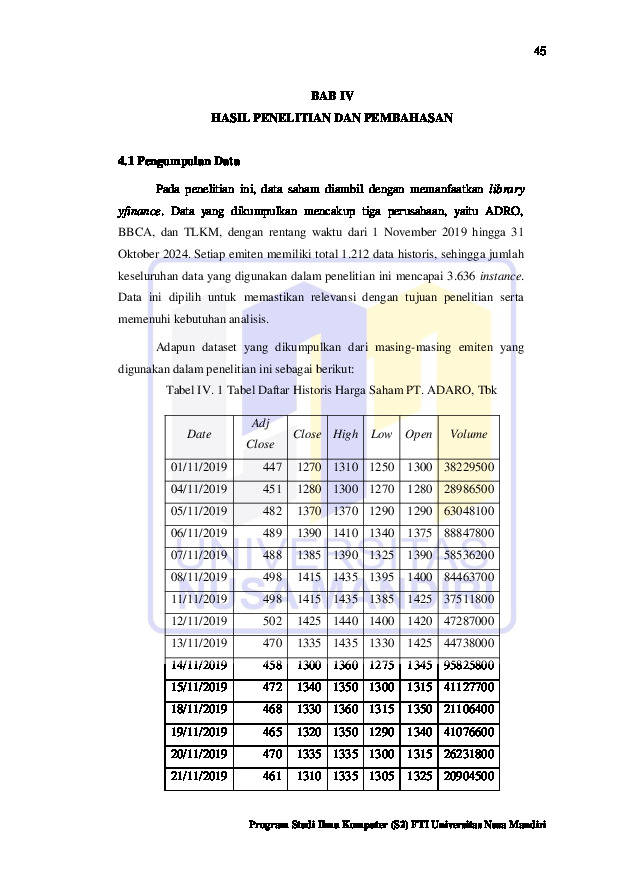

Data historis saham diperoleh dari Yahoo Finance untuk periode November 2019

hingga Oktober 2024. Penelitian melibatkan preprocessing data, normalisasi,

pembagian data latih dan uji (80:20), serta evaluasi menggunakan metrik Root Mean

Squared Error (RMSE) dan Mean Absolute Percentage Error (MAPE). Hasil

menunjukkan GRU memiliki performa terbaik, dengan RMSE terendah (ADRO:

69.36, BBCA: 83.03, TLKM: 111.97) dan MAPE terendah (ADRO: 2.3%, BBCA:

2.3%, TLKM: 4.1%) dibandingkan LSTM dan Bi-LSTM. GRU direkomendasikan

sebagai model yang optimal untuk prediksi harga saham di pasar modal Indonesia

Unduhan

-

-

14220017_Laura.pdf

Terakhir download 28 Jul 2026 23:07Tesis keseluruhan

- diunduh 4x | Ukuran 3,195,372

-

-

DAFTAR REFERENSI.pdf

Terakhir download 04 Aug 2026 12:08Daftar referensi

- diunduh 243x | Ukuran 213,804

-

HALAMAN JUDUL LAPORAN TESIS.pdf

Terakhir download 02 Aug 2026 11:08Cover

- diunduh 149x | Ukuran 26,185

-

REFERENSI

1. A. Nilsen, “Perbandingan Model RNN, Model LSTM, dan Model GRU dalam Memprediksi Harga Saham-Saham LQ45,” J. Stat. Dan Apl., vol. 6, no. 1, pp. 137–147, Jun. 2022, doi: 10.21009/JSA.06113.

2. D. Desyanti, J. Suarlin, and R. Faisal, “Otoritas Guru Dalam Prestasi Belajar Siswa Menggunakan Fuzzy Mamdani,” J. MEDIA Inform. BUDIDARMA, vol. 7, no. 3, p. 1323, Jul. 2023, doi: 10.30865/mib.v7i3.6368.

3. K. Kwanda, D. E. Herwindiati, and M. D. Lauro, “Perbandingan LSTM dan Bidirectional LSTM pada Sistem Prediksi Harga Saham Berbasis Website,” Ranah Res. J. Multidiscip. Res. Dev., vol. 7, no. 1, pp. 26–35, Nov. 2024, doi: 10.38035/rrj.v7i1.1255.

4. N. W. Meri Aryati, I. K. A. G. Wiguna, N. W. S. Putri, I. K. K. Widiartha, and N. L. W. S. R. Ginantra, “Komparasi Metode LSTM dan GRU dalam Memprediksi Harga Saham,” J. MEDIA Inform. BUDIDARMA, vol. 8, no. 2, p. 1131, Apr. 2024, doi: 10.30865/mib.v8i2.7342.

5. A. Wiejaya and I. Fenriana, “Prediksi Harga Saham Top 10 NASDAQ dengan Time Series Prophet,” Bit-Tech, vol. 7, no. 2, pp. 252–262, Dec. 2024, doi: 10.32877/bt.v7i2.1736.

6. V. Marlisa, S. Suminar, T. Ariana, D. L. Rera, and Ratnasari, “Profitabilitas Sebagai Mediasi Struktur Modal dan Pertumbuhan Perusahaan Terhadap Return Saham Syariah: Profitability as a Mediation of Capital Structure and Company Growth on Sharia Stock Return,” EKOMABIS J. Ekon. Manaj. Bisnis, vol. 2, no. 02, pp. 113–124, Jul. 2021, doi: 10.37366/ekomabis.v2i02.194.

7. M. Batubara, S. Yuni Lubis, and P. Wati, “Pengaruh Rasio Keuangan Terhadap Harga Saham Syariah pada PT. Akr Corporindo,” Rayah Al-Islam, vol. 7, no. 3, pp. 1495–1513, Dec. 2023, doi: 10.37274/rais.v7i3.863.

8. E. Sunardi, “Seberapa Kuat Pengaruh Perubahan Kurs, Suku Bunga, Pertumbuhan Ekonomi, Transaksi Asing, Efisiensi, Produktivitas, Total Asset Turn Over, dan Return On Equity Terhadap Perubahan Harga Saham PT Semen Indonesia (Persero), Tbk.,” Respati, vol. 15, no. 3, p. 52, Dec. 2020, doi: 10.35842/jtir.v15i3.372.

9. D. Doman and N. Doman, “Penerapan Prinsip Pembangunan Berkelanjutan dan Ekonomi Berwawasan dalam Peraturan Perundang-Undangan Penggunaan Kawasan Hutan dalam Rangka PSN Pasca Pengesahan Perpres 66/2020,” J. Huk. Lingkung. Indones., vol. 7, no. 1, pp. 71–97, Dec. 2020, doi: 10.38011/jhli.v7i1.222.

10. B. Sugianto, D. Kurniawati, and Z. Abbas, “OTONOMI DAERAH DAN PELUANG INVESTASI UNTUK PERCEPATAN PEMBANGUNAN,” Lex Libr. J. Ilmu Huk., p. 66, Nov. 2020, doi: 10.46839/lljih.v0i0.286.

11. M. D. Palguno, D. Valeriani, and S. Suhartono, “Pengaruh Pendapatan Asli Daerah dan belanja modal terhadap pertumbuhan ekonomi Provinsi Kepulauan Bangka Belitung tahun 2009-2018,” SOROT, vol. 15, no. 2, p. 105, Oct. 2020, doi: 10.31258/sorot.15.2.105-116.

12. Maudi Sari Mawardi, Susilo Setiyawan, and Rizka Estisia Pratiwi, “Analisis Harga Wajar Saham dengan Dividend Discount Model pada Perusahaan Sektor Keuangan,” J. Ris. Manaj. Dan Bisnis, pp. 86–92, Dec. 2023, doi: 10.29313/jrmb.v3i2.2874.

13. C. I. Muslih, “Pengaruh Laba, Nilai Buku dan CSR Terhadap Harga Saham Perusahaan Terdaftar pada Jakarta Islamic Index 70 (JII70) Tahun 2019-2021,” KONSTELASI Konvergensi Teknol. Dan Sist. Inf., vol. 3, no. 1, pp. 174–183, Jun. 2023, doi: 10.24002/konstelasi.v3i1.7085.

14. A. Surahman, N. Rusnaeni, and M. Mas’adi, “PENGARUH DARI DEGREE OPERATING LEVERAGE TERHADAP KEBIJAKAN PEMBAGIAN DIVIDEN PT. ASTRA INTERNASIONAL,” J. Sekr. Univ. Pamulang, vol. 9, no. 2, p. 125, Jul. 2022, doi: 10.32493/skr.v9i2.21925.

15. A. Bagaswara and L. N. Wati, “PENGARUH FAKTOR INTERNAL DAN EKSTERNAL TERHADAP RETURN SAHAM DENGAN MODERASI GOOD CORPORATE GOVERNANCE (GCG),” J. Ekobis Ekon. Bisnis Manaj., vol. 10, no. 2, pp. 263–277, Sep. 2020, doi: 10.37932/j.e.v10i2.145.

16. X. Lin, “The Limitations of the Efficient Market Hypothesis,” Highlights Bus. Econ. Manag., vol. 20, pp. 37–41, Nov. 2023, doi: 10.54097/hbem.v20i.12311.

17. H. Altin, “Efficient Market Hypothesis for Islamic Capital Markets:,” in Advances in Finance, Accounting, and Economics, A. Rafay, Ed., IGI Global, 2019, pp. 489–523. doi: 10.4018/978-1-7998-0218-1.ch027.

18. X. Brouty and M. Garcin, “A statistical test of market efficiency based on information theory,” Quant. Finance, vol. 23, no. 6, pp. 1003–1018, Jun. 2023, doi: 10.1080/14697688.2023.2211108.

19. K. Nyakurukwa and Y. Seetharam, “Alternatives to the efficient market hypothesis: an overview,” J. Cap. Mark. Stud., vol. 7, no. 2, pp. 111–124, Dec. 2023, doi: 10.1108/JCMS-04-2023-0014.

20. B. Jamalpur, “DATA EXPLORATION AS A PROCESS OF KNOWLEDGE FINDING AND THE ROLE OF MINING DATA TOWARDS INFORMATION SECURITY,” J. Mech. Contin. Math. Sci., vol. 15, no. 6, Jun. 2020, doi: 10.26782/jmcms.2020.06.00017.

21. A. A. Maryoosh and E. M. Hussein, “A Review: Data Mining Techniques and Its Applications,” Int. J. Comput. Sci. Mob. Appl., vol. 10, no. 3, pp. 1–14, Mar. 2022, doi: 10.47760/ijcsma.2022.v10i03.001.

22. G. Kaderye, A. Arif, and R. Kundu, “Data Mining in Different Fields: A Study,” Int. J. Innov. Sci. Res. Technol. IJISRT, pp. 1828–1838, Apr. 2024, doi: 10.38124/ijisrt/IJISRT24MAR1384.

23. S. M. Dol, “Use of Classification Technique in Educational Data Mining,” in 2021 4th Biennial International Conference on Nascent Technologies in Engineering (ICNTE), NaviMumbai, India: IEEE, Jan. 2021, pp. 1–7. doi: 10.1109/ICNTE51185.2021.9487739.

24. R. Ribeiro, A. Pilastri, C. Moura, F. Rodrigues, R. Rocha, and P. Cortez, “Predicting the Tear Strength of Woven Fabrics Via Automated Machine Learning: An Application of the CRISP-DM Methodology:,” in Proceedings of the 22nd International Conference on Enterprise Information Systems, Prague, Czech Republic: SCITEPRESS - Science and Technology Publications, 2020, pp. 548–555. doi: 10.5220/0009411205480555.

25. L.-H. Le, “Time series analysis and applications in data analysis, forecasting and prediction,” HPU2 J. Sci. Nat. Sci. Technol., vol. 3, no. 1, pp. 20–29, Apr. 2024, doi: 10.56764/hpu2.jos.2024.3.1.20-29.

26. D. Chicco, M. J. Warrens, and G. Jurman, “The coefficient of determination R-squared is more informative than SMAPE, MAE, MAPE, MSE and RMSE in regression analysis evaluation,” PeerJ Comput. Sci., vol. 7, p. e623, Jul. 2021, doi: 10.7717/peerj-cs.623.

27. Y. Chen and J. Li, “Recurrent Neural Networks algorithms and applications,” in 2021 2nd International Conference on Big Data & Artificial Intelligence & Software Engineering (ICBASE), Zhuhai, China: IEEE, Sep. 2021, pp. 38–43. doi: 10.1109/ICBASE53849.2021.00015.

28. G. Neves, J.-B. Chaudron, and A. Dion, “Recurrent Neural Networks Analysis for Embedded Systems:,” in Proceedings of the 13th International Joint Conference on Computational Intelligence, Valletta, Malta: SCITEPRESS - Science and Technology Publications, 2021, pp. 374–383. doi: 10.5220/0010715700003063.

29. G. Van Houdt, C. Mosquera, and G. Nápoles, “A review on the long short-term memory model,” Artif. Intell. Rev., vol. 53, no. 8, pp. 5929–5955, Dec. 2020, doi: 10.1007/s10462-020-09838-1.

30. N. B. Erichson, S. H. Lim, and M. W. Mahoney, “Gated Recurrent Neural Networks with Weighted Time-Delay Feedback,” 2022, arXiv. doi: 10.48550/ARXIV.2212.00228.

31. S.-L. Shen, P. G. Atangana Njock, A. Zhou, and H.-M. Lyu, “Dynamic prediction of jet grouted column diameter in soft soil using Bi-LSTM deep learning,” Acta Geotech., vol. 16, no. 1, pp. 303–315, Jan. 2021, doi: 10.1007/s11440-020-01005-8.

32. M. Ćalasan, S. H. E. Abdel Aleem, and A. F. Zobaa, “On the root mean square error (RMSE) calculation for parameter estimation of photovoltaic models: A novel exact analytical solution based on Lambert W function,” Energy Convers. Manag., vol. 210, p. 112716, Apr. 2020, doi: 10.1016/j.enconman.2020.112716.

33. H. Zhou et al., “Low-Complexity Double-Vector Model Predictive Control With Minimum Root Mean Square Error for Three-Phase Three-Level Inverters,” IEEE J. Emerg. Sel. Top. Power Electron., vol. 11, no. 6, pp. 5809–5819, Dec. 2023, doi: 10.1109/JESTPE.2023.3323550.

34. H.-J. Lee, C.-C. Lee, Y.-M. Yang, W.-Y. Lee, and C.-H. Kuan, “Enhanced Fourier Series for Precise Signal Analysis,” in 2024 Photonics & Electromagnetics Research Symposium (PIERS), Chengdu, China: IEEE, Apr. 2024, pp. 1–5. doi: 10.1109/PIERS62282.2024.10618403.

35. D. Kurniasari, M. E. Nuraini, W. Wamiliana, and R. K. Nisa, “A Case Study: Comparison of LSTM and GRU Methods for Forecasting Oil, Non-Oil, and Gas Export Values in Indonesia,” J. Tek. Inform., vol. 17, no. 2, pp. 127–138, Oct. 2024, doi: 10.15408/jti.v17i2.39098.

36. D. E. Herwindiati, J. Hendryli, and N. H. Sarmin, “A Comparison of Two Deep Learning Models on The Stock Exchange Predictions”.

37. M. F. Fayyad, V. Kurniawan, M. R. Anugrah, B. H. Estanto, and T. Bilal, “Application of Recurrent Neural Network Bi-Long Short-Term Memory, Gated Recurrent Unit and Bi-Gated Recurrent Unit for Forecasting Rupiah Against Dollar (USD) Exchange Rate,” Public Res. J. Eng. Data Technol. Comput. Sci., vol. 2, no. 1, pp. 1–10, Apr. 2024, doi: 10.57152/predatecs.v2i1.1094.

38. C. Han and X. Fu, “Challenge and Opportunity: Deep Learning-Based Stock Price Prediction by Using Bi-Directional LSTM Model,” Front. Bus. Econ. Manag., vol. 8, no. 2, pp. 51–54, Apr. 2023, doi: 10.54097/fbem.v8i2.6616.

39. S. Özer and Ü. N. Erol, “Electric Vehicle Stock Price Prediction using LSTM, Bi-LSTM and GRU,” in 2024 8th International Artificial Intelligence and Data Processing Symposium (IDAP), Malatya, Turkiye: IEEE, Sep. 2024, pp. 1–7. doi: 10.1109/IDAP64064.2024.10710919.

40. P. L. Seabe, C. R. B. Moutsinga, and E. Pindza, “Forecasting Cryptocurrency Prices Using LSTM, GRU, and Bi-Directional LSTM: A Deep Learning Approach,” Fractal Fract., vol. 7, no. 2, p. 203, Feb. 2023, doi: 10.3390/fractalfract7020203.

41. M. R. Nurhambali, Y. Angraini, and A. Fitrianto, “Implementation of Long Short-Term Memory for Gold Prices Forecasting,” Malays. J. Math. Sci., vol. 18, no. 2, pp. 399–422, Jun. 2024, doi: 10.47836/mjms.18.2.11.

42. N. K. Khairunisa and P. Hendikawati, “Long Short-Term Memory and Gated Recurrent Unit Modeling for Stock Price Forecasting,” J. Mat. Stat. Dan Komputasi, vol. 21, no. 1, pp. 321–333, Sep. 2024, doi: 10.20956/j.v21i1.35930.

43. M. I. Pramesti, F. I. Indikawati, and A. Prahara, “Multivariate time series stock price data prediction in the banking sector in Indonesia using Bidirectional Long Short-Term Memory (biLSTM),” vol. 4, no. 2, 2022.

44. A. P. Meriani and A. Rahmatulloh, “PERBANDINGAN GATED RECURRENT UNIT (GRU) DAN ALGORITMA LONG SHORT TERM MEMORY (LSTM) LINEAR REFRESSION DALAM PREDIKSI HARGA EMAS MENGGUNAKAN MODEL TIME SERIES,” J. Inform. Dan Tek. Elektro Terap., vol. 12, no. 1, Jan. 2024, doi: 10.23960/jitet.v12i1.3808.

45. D. Satria, “PREDICTING BANKING STOCK PRICES USING RNN, LSTM, AND GRU APPROACH,” Appl. Comput. Sci., vol. 19, no. 1, pp. 82–94, Mar. 2023, doi: 10.35784/acs-2023-06.

46. R. A. Fahrezi, M. Y. Wijaya, and N. Fitriyati, “PREDIKSI HARGA PENUTUPAN SAHAM BANK CENTRAL ASIA: IMPLEMENTASI ALGORITMA LONG SHORT-TERM MEMORY DAN PERBANDINGANNYA DENGAN SUPPORT VECTOR MACHINE,” J. Lebesgue J. Ilm. Pendidik. Mat. Mat. Dan Stat., vol. 5, no. 1, pp. 452–464, Apr. 2024, doi: 10.46306/lb.v5i1.582.

47. M. N. Wathani, K. Kusrini, and K. Kusnawi, “Prediksi Tren Pergerakan Harga Saham PT Bank Central Asia Tbk, Dengan Menggunakan Algoritma Long Shot Term Memory (LSTM),” Infotek J. Inform. Dan Teknol., vol. 6, no. 2, pp. 502–512, Jul. 2023, doi: 10.29408/jit.v6i2.19824.

48. H. Nazhiroh, Dina Fitria, Dony Permana, and Zilrahmi, “PT.Telkom (Tbk) Stock Price Forecasting Using Long Short Term Memory (LSTM),” UNP J. Stat. Data Sci., vol. 2, no. 4, pp. 414–421, Nov. 2024, doi: 10.24036/ujsds/vol2-iss4/223.

49. Gajayana University, Malang, F. Poernamawatie, I. N. Susipta, Gajayana University, Malang, D. Winarno, and Gajayana University, Malang, “Sharia Bank of Indonesia Stock Price Prediction using Long Short-Term Memory,” J. Econ. Finance Manag. Stud., vol. 07, no. 07, Jul. 2024, doi: 10.47191/jefms/v7-i7-94.

50. D. Rudhistiar, M. H. Wahyudi, W. Wahyani, and T. A. S. Yusri, “STOCK PRICE PREDICTION FOR BANK SYARIAH INDONESIA USING BIDIRECTIONAL LONG SHORT-TERM MEMORY (BI-LSTM),” Int. J. Comput. Sci. Inf. Technol., 2024.

51. T. Baihaqi, M. A. Sugiyarto, R. P. Daksa, F. I. Kurniadi, M. Fakhruddin, and H. Erandi, “Unveling the Precision of Deep Learning Models for Stock Price Prediction: A Comparative Analysis of Bi-LSTM, LSTM, and GRU,” in 2023 International Conference on Converging Technology in Electrical and Information Engineering (ICCTEIE), Bandar Lampung, Indonesia: IEEE, Oct. 2023, pp. 61–64. doi: 10.1109/ICCTEIE60099.2023.10366646.

Kiriman Terbaru

-

05 Aug 2026

-

03 Aug 2026

-

03 Aug 2026

-

03 Aug 2026

-

03 Aug 2026