- 05 Nov

- 2024

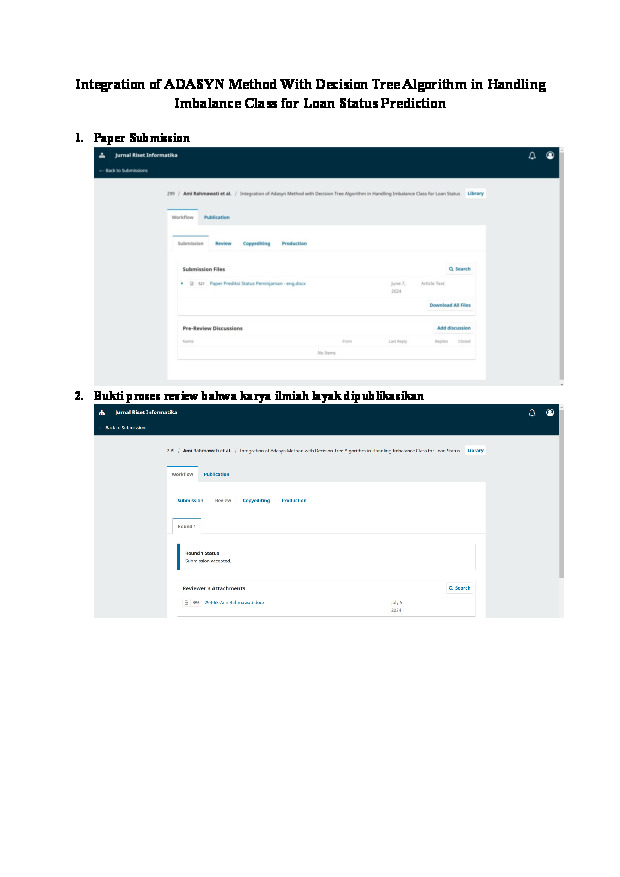

Integration of ADASYN Method With Decision Tree Algorithm In Handling Imbalance Class For Loan Status Prediction

Determining the provision of credit is generally carried out based on measuring credibility using credit analysis principles (5C principles). However, this method requires quite a long processing time and is very susceptible to subjective judgments which might influence the final results. This research aims to utilize data mining techniques by developing modeling on loan status prediction datasets. The stages in this research include data preprocessing, modeling and evaluation using accuracy metrics and ROC graphs. In this analysis, it is known that there is a class imbalance in the processed dataset so it is necessary to carry out an oversampling technique. In this research, the ADASYN (Adaptive Synthetic) Oversampling technique is used to ensure the class distribution is more balanced. Then, the ADASYN technique is integrated with the Decision Tree Algorithm to build a prediction model. The research results show that the two methods are able to increase prediction accuracy by 12.22% from 73% to 85.22%. This improvement was obtained by comparing the accuracy results before and after using the ADASYN Oversampling technique. This finding is important because it proves that the implementation of such integration modeling can significantly improve the performance of classification models and can provide strong potential for practical application in helping more effective loan status predictions.

Unduhan

-

Integration Of Adasyn Method with Decision Tree Algorithm In Handling Imbalance Class For Loan Status Prediction.pdf

Terakhir download 19 Mar 2026 14:03Integration of ADASYN Method With Decision Tree Algorithm In Handling Imbalance Class For Loan Status Prediction

- diunduh 342x | Ukuran 761 KB

-

Dokumen Bukti Korespondensi_Genap 2324.pdf

Terakhir download 01 Mar 2026 13:03Bukti Dokumen Bukti Korespondensi_Genap 2324

- diunduh 92x | Ukuran 442 KB

REFERENSI

[1] M. Eltania, “Pengaruh Suku Bunga Kredit, Inflasi, Dan Nilai Tukar Terhadap Jenis Penyaluran Kredit,” Contemp. Stud. Econ. Financ. Bank., vol. 1 NO 1, no. 1, pp. 25–37, 2022.

[2] F. Yenila, H. Marfalino, and S. Defit, “Model Analisis Machine Learning dengan Pendekatan Deep Learning dalam Penentuan Kolektabilitas,” JST (Jurnal Sains dan Teknol., vol. 12, no. 2, pp. 403–414, 2023, doi: 10.23887/jstundiksha.v12i2.54035.

[3] Badan Pusat Statistik, “Posisi Kredit Perbankan Menurut Jenis Penggunaan Pada Bank Pemerintah (Juta Rupiah),” BPS, 2019. https://ppukab.bps.go.id/indicator/105/158/1/posisi-kredit-perbankan-menurut-jenis-penggunaan-pada-bank-pemerintah-.html (accessed Apr. 11, 2024).

[4] GAO Report, “Pandemic Assistance Likely Helped Reduce Balances, and Credit Terms Varied Among Demographic Groups,” U.S. Government Accountability Office, 2023. https://www.gao.gov/products/gao-23-105269

[5] I. Ubaedi and Y. M. Djaksana, “Optimasi Algoritma C4.5 Menggunakan Metode Forward Selection Dan Stratified Sampling Untuk Prediksi Kelayakan Kredit,” JSiI (Jurnal Sist. Informasi), vol. 9, no. 1, pp. 17–26, 2022, doi: 10.30656/jsii.v9i1.3505.

[6] F. F. Hermawan and Y. Yamasari, “Implementasi K-Nearest Neighbor dengan Pemilihan Fitur pada Aplikasi Prediksi Kelayakan Pengajuan Pinjaman,” J. Informatics Comput. Sci., vol. 3, no. 04, pp. 411–424, 2022, doi: 10.26740/jinacs.v3n04.p411-424.

[7] A. Prawira, D. Arisandi, and T. Sutrisno, “Penerapan Algoritma Naive Bayes dan Multiple Linear Regression Untuk Prediksi Status dan Plafon Kredit (Studi Kasus: Bank ABC),” J. Educ., vol. 5, no. 1, pp. 1075–1087, 2022, doi: 10.31004/joe.v5i1.720.

[8] I. F. Tarigan, D. Hartama, Suhada, Saifullah, and I. S. Saragih, “Penerapan Data Mining Pada Prediksi Kelayakan Pemohon Kredit Mobil Dengan K-Medoids Clustering,” KLIK Kaji. Ilm. Inform. …, vol. 1, no. 4, pp. 170–179, 2021, [Online]. Available: http://www.djournals.com/klik/article/view/153

[9] S. Syafudin, R. A. Nugraha, K. Handayani, W. Gata, and S. Linawati, “Prediksi Status Pinjaman Bank dengan Deep Learning Neural Network (DNN),” J. Tek. Komput. AMIK BSI, vol. 7, no. 2, pp. 130–135, 2021.

[10] A. A. Pratiwi, W. T. Saraswati, R. F. Ardiansyah, E. H. Rouf, and R. A. Pratama, “Determining The Loan Feasiblity of Bank Customers Using Naïve Bayes, K-Nearest Neighbors And Linear Regression Algorithms,” J. Ilmu Komput. dan Sist. Inf., vol. 6, no. 3, pp. 226–236, 2023.

[11] I. Nurdiyanto, O. Nurdiawan, A. Irma Purnamasari, and D. Ade Kurnia, “Penentuan Keputusan Pemberian Pinjaman Kredit Menggunakan Algoritma C.45,” J. Dadta Sci. dan Inform., vol. 2, no. 1, pp. 1–5, 2022.

[12] R. Sitepu and M. Manohar, “Implementasi Algoritma K-Nearest Neigbor Untuk Klasifikasi Pengajuan Kredit,” J. Sist. Informasi, Tek. Inform. dan Teknol. Pendidik., vol. 1, no. 2, pp. 49–56, 2022, doi: 10.55338/justikpen.v1i2.6.

[13] B. Prasojo and E. Haryatmi, “Analisa Prediksi Kelayakan Pemberian Kredit Pinjaman dengan Metode Random Forest,” J. Nas. Teknol. dan Sist. Inf., vol. 7, no. 2, pp. 79–89, 2021, doi: 10.25077/teknosi.v7i2.2021.79-89.

[14] I. Pratama, A. Y. Chandra, and P. T. Presetyaningrum, “Seleksi Fitur dan Penanganan Imbalanced Data menggunakan RFECV dan ADASYN,” J. Eksplora Inform., vol. 11, no. 1, pp. 38–49, 2022, doi: 10.30864/eksplora.v11i1.578.

[15] J. Al Amien, Yoze Rizki, and Mukhlis Ali Rahman Nasution, “Implementasi Adasyn Untuk Imbalance Data Pada Dataset UNSW-NB15 Adasyn Implementation For Data Imbalance on UNSW-NB15 Dataset,” J. CoSciTech (Computer Sci. Inf. Technol., vol. 3, no. 3, pp. 242–248, 2022, doi: 10.37859/coscitech.v3i3.4339.

[16] A. P. Monika, F. E. P. Risti, I. Binanto, and N. F. Sianipar, “Perbandingan Algoritma Klasifikasi Random Forest , Gaussian Naive Bayes , dan K-Nearest Neighbor untuk Data Tidak Seimbang dan Data yang diseimbangkan dengan Metode Adaptive Synthetic pada Dataset LCMS Tanaman Keladi Tikus,” J. Semin. Nas. Tek. Elektro, Inform. Sist. Inf., pp. 3–7, 2023.

[17] W. Hidayat, M. Ardiansyah, and A. Setyanto, “Pengaruh Algoritma ADASYN dan SMOTE terhadap Performa Support Vector Machine pada Ketidakseimbangan Dataset Airbnb,” Edumatic J. Pendidik. Inform., vol. 5, no. 1, pp. 11–20, 2021, doi: 10.29408/edumatic.v5i1.3125.

Kiriman Terbaru

-

17 Mar 2026

-

17 Mar 2026

-

17 Mar 2026

-

17 Mar 2026

-

15 Mar 2026